In this era of global village, people frequently send international money transfers to support their families, fund education, or execute business deals. International money transfer sounds great, but unfortunately, less glamorous is the regularity that comes with taxes on such international transactions. Indeed, because recent changes in those tax laws leave most people scratching their heads, it is important to understand the Foreign Remittance Tax for the convenience of traversing the Indian financial landscape. In this blog, we will take an in-depth look at the specifics of the Foreign Remittance Tax, identify the numbers that lie at the heart of this change, bring you the very latest updates and exemptions, and share smart strategies that will help keep more of your money where it should be: in your pocket.

Who Was the Key Person Behind These Changes?

Recent changes in Foreign Remittance Tax by India bore the imprint of top financial policymakers, including Finance Minister Nirmala Sitharaman. Those steps are part of the entirety: being devised for better regulation of foreign remittances to make sure the money going out of the country is accounted for and taxed as necessary. The focus of the government still remains to increase the tax compliance and to ensure that untaxed income should not sneak out of the country’s borders. These amendments go a long way toward helping in their cause.

Save big on your every international money transfer!

Send money at the lowest exchange rates & ZERO convenience fees with moneyHOP.

New Updates on Foreign Remittance Tax in India

The Indian government has introduced several significant revisions to the taxation system for foreign remittances:

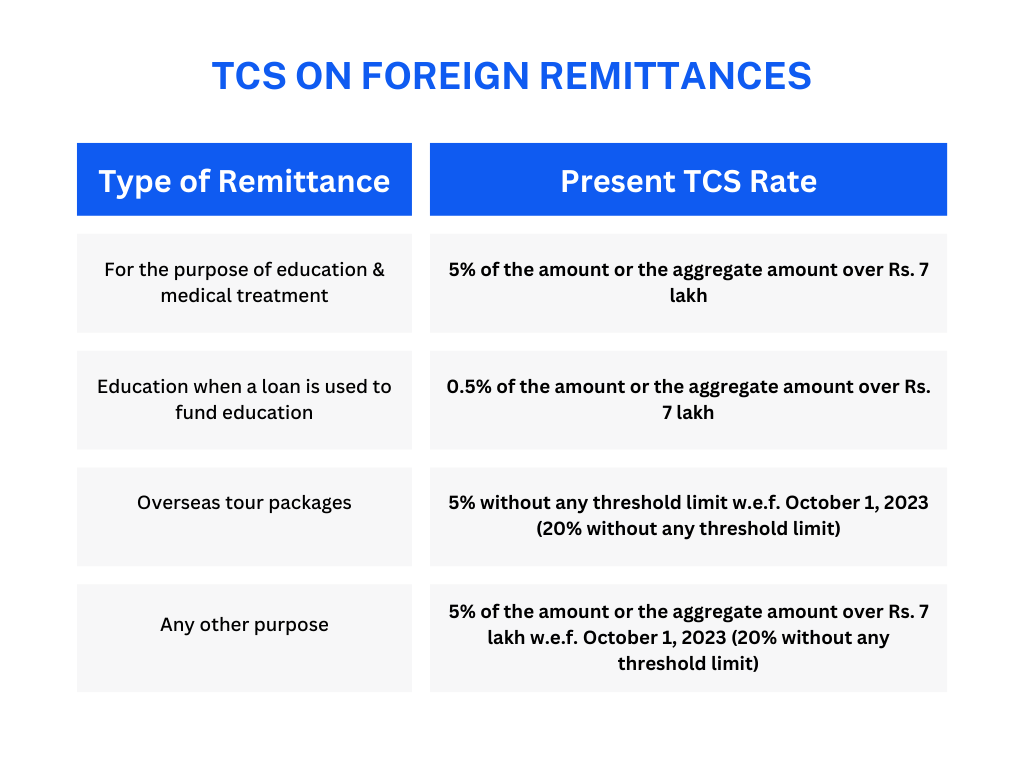

- TCS on Foreign Remittances: One of the major updates is the increase in Tax Collected at Source (TCS) for foreign remittances under the Liberalized Remittance Scheme (LRS). The TCS rate has surged from 5% to 20% for all foreign remittances that exceed ₹7 lakh within a single financial year. This adjustment impacts various forms of transactions, including overseas travel, educational expenses abroad, and international investments.

- Exemptions for Education and Medical Treatment: The government has provided relief for students and those seeking medical treatment abroad. For education-related remittances funded through loans, the TCS rate remains at 5% for amounts above ₹7 lakh. Similarly, remittances for medical treatment are also taxed at 5%.

- Impact on High Net-Worth Individuals: The TCS provision has been affecting in particular high net worth individuals who invariably invest in foreign assets or remit large sums abroad. This has been initiated so that large amounts are not paid out without proper tax documentation.

Tax Implications on Foreign Remittances

The nature and purpose of the foreign remittance are what determine taxability. Here’s what you need to know:

- Personal Remittances: The TCS shall be attracted, in case remittance of money is abroad for purposes such as family or friends, and if the amount exceeds ₹7 lakh in the year.

- Investment Abroad: In the case of investment in foreign shares, bonds, or real estate, you will be liable to pay TCS if your investment exceeds the limit; tax is collected at source on remittance.

- Educational Expenses: Students going abroad for higher studies can remit funds under the LRS. If the amount exceeds ₹7 lakh, the applicable TCS will be 5%, provided it is funded by an educational loan.

- Medical Treatment: Similar to education, remittances for medical treatment are taxed at 5% for amounts above ₹7 lakh.

- Gifts: If you are sending money abroad as a gift, it will attract TCS if the amount exceeds the threshold.

Table of Present TCS Rates on Foreign Remittances

Exemptions

While the TCS rules are stringent, there are certain exemptions and reliefs provided by the government:

- Remittances Below ₹7 Lakh: Any remittance under ₹7 lakh in a financial year is exempt from TCS, regardless of the purpose.

- Education Loans: As mentioned, education-related remittances funded by loans attract a lower TCS rate of 5%.

- Medical Treatment: Remittances for medical treatment abroad are also subject to a lower TCS rate of 5%.

How moneyHOP is Helping in Foreign Remittances?

moneyHOP is committed to making foreign remittances seamless and cost-effective, especially in light of the new tax regulations. Here’s how moneyHOP is assisting:

- Transparent Fee Structure: moneyHOP maintains a clear fee structure, keeping you informed of all costs involved from the start, including any taxes that would be applicable.

- Efficient Transfers: With moneyHOP, you can execute international transfers quickly and efficiently, avoiding delays that could potentially increase costs.

- Expert Guidance: moneyHOP has expert guidance on how to maneuver through the complications of foreign remittance taxes so that a person can make informed decisions.

- Innovative Solutions: moneyHOP provides secure and compliance-ready solutions for foreign remittance to ensure your money travels safely and cost-effectively.

Why pay more for international money transfers when moneyHOP is here?

- NO hidden fees

- ZERO convenience fees

- Real-time updates

- Lowest exchange rates

Final Thoughts

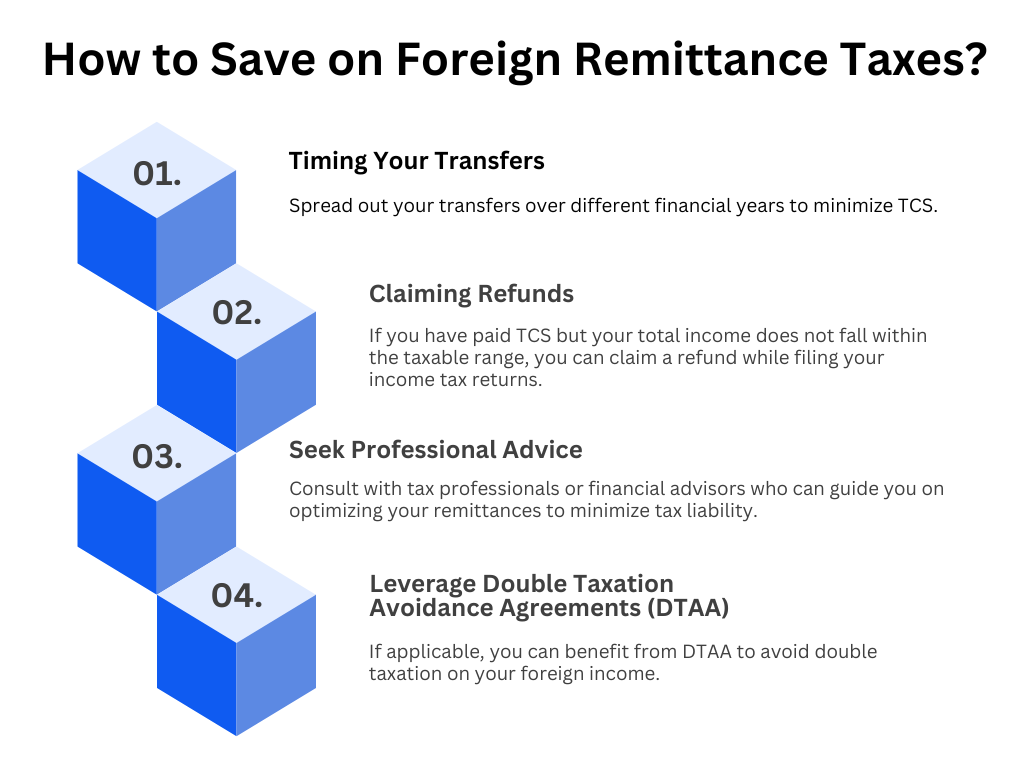

Now, addressing the challenges of Foreign Remittance Tax may seem pretty huge at first; when the right set of strategies and tools falls into place, it simply becomes achievable. Keep yourself abreast on latest updates of regulatory mechanisms, plan the proper transfer right, and use services like moneyHOP to make your international transactions efficient and cost-effective. After all, it is not just about moving the money, but doing so intelligently. Having the right approach means you can easily turn what seems to be a very complex process into an easy experience and work in your favor.

Leave a Reply